Navigating 2024 taxes involves understanding emerging technologies, geopolitical risks, and economic shifts, alongside traditional brackets and credits—a complex landscape for taxpayers․

The 2024 tax season arrives amidst a backdrop of global uncertainty, marked by economic shifts, technological advancements, and evolving geopolitical landscapes․ As we move further into a world shaped by rapid change, understanding the nuances of the tax code becomes increasingly crucial for individuals and businesses alike․ Key issues impacting taxpayers this year include the continued influence of inflation, the growth of the gig economy, and the rise of artificial intelligence․

The World Economic Forum’s reports highlight risks from misinformation and climate change, factors indirectly influencing economic stability and, consequently, tax implications․ Furthermore, the increasing prevalence of digital platforms and freelance work necessitates a clear understanding of self-employment taxes and reporting requirements․ Staying informed about these trends and utilizing available resources will be essential for a smooth and compliant tax filing experience in 2024․

Key Tax Brackets for 2024

As inflation cools, the 2024 tax brackets reflect relatively slight adjustments, impacting how income is taxed across different levels․ While specific rates remain largely consistent with prior years, understanding these brackets is fundamental for accurate tax planning․ These adjustments are crucial given the broader economic context, including geoeconomic fragmentation and ongoing economic uncertainty highlighted in recent reports․

Taxpayers should consult the official IRS guidelines for precise bracket thresholds based on filing status (single, married filing jointly, etc․)․ These brackets determine the progressive tax system, where higher income portions are taxed at higher rates․ Considering these changes alongside potential tax credits and deductions is vital for minimizing tax liability․ Staying informed about these adjustments, within the context of a changing global landscape, is key for effective financial management throughout 2024․

Standard Deduction Amounts ― 2024

The standard deduction for 2024 offers a simplified alternative to itemizing deductions, reducing taxable income for millions of taxpayers․ These amounts are adjusted annually to account for inflation, providing some relief amidst broader economic shifts․ Understanding these figures is crucial, especially considering the current climate of economic uncertainty and the potential impact of geoeconomic fragmentation․

For single filers, the standard deduction is significantly higher than in previous years․ Married couples filing jointly receive a larger deduction, and heads of households also benefit from increased amounts․ Taxpayers aged 65 or older, or those who are blind, receive an additional standard deduction․ Choosing between the standard deduction and itemizing depends on individual circumstances; carefully evaluating both options is essential for maximizing tax savings in 2024, given the evolving financial landscape․

Itemized Deductions: A Quick Overview

Itemized deductions allow taxpayers to reduce their taxable income by listing eligible expenses, potentially resulting in greater tax savings than the standard deduction․ However, navigating these deductions requires careful record-keeping and understanding of current regulations, especially with emerging technologies impacting financial tracking․

Common itemized deductions include medical expenses exceeding a certain percentage of adjusted gross income, state and local taxes (SALT), and mortgage interest․ The availability and limitations of these deductions can be complex, influenced by factors like economic uncertainty and legislative changes․ Determining whether to itemize versus taking the standard deduction requires a thorough assessment of individual financial circumstances․ Considering the broader economic context, including inflation and geopolitical risks, is vital for optimizing tax strategy in 2024․

Medical Expense Deduction

The medical expense deduction allows taxpayers to deduct qualified medical expenses exceeding 7․5% of their Adjusted Gross Income (AGI)․ This deduction encompasses costs for diagnosis, treatment, prevention of disease, and insurance premiums․ With healthcare system transformations being a key issue in 2024, understanding eligible expenses is crucial․

Qualified medical expenses include doctor visits, hospital stays, prescription drugs, and even certain home improvements made for medical reasons․ Detailed records are essential, as substantiation is required․ The rise of telehealth and innovative medical technologies may introduce new expense categories․ Considering potential health impacts from climate change, proactive healthcare spending could become more significant․ Navigating these complexities requires careful attention to IRS guidelines and potentially professional tax advice, especially given the evolving healthcare landscape and economic uncertainties․

State and Local Tax (SALT) Deduction

The State and Local Tax (SALT) deduction allows taxpayers to deduct some of the taxes they pay to state and local governments․ However, the Tax Cuts and Jobs Act of 2017 placed a $10,000 limit on this deduction, impacting many, particularly those in high-tax states․ Understanding this limitation is vital for 2024 tax planning․

Eligible taxes include property taxes, state and local income taxes (or sales taxes if you choose to itemize instead of taking the standard deduction)․ Given the geoeconomic fragmentation and economic uncertainty of 2024, state and local tax policies may experience changes․ Taxpayers should carefully track their payments and consider whether itemizing deductions, including SALT, exceeds the standard deduction amount․ The interplay between federal tax laws and state/local fiscal policies creates a complex situation, requiring diligent record-keeping and potentially professional guidance to maximize potential savings․

Tax Credits for 2024

Tax credits directly reduce your tax liability, offering a more significant benefit than deductions․ For 2024, several key credits are available to eligible taxpayers, potentially easing the burden amidst economic uncertainty and inflation․ These include credits related to family expenses and income levels․

The Child Tax Credit continues to be a vital support for families, though updates to eligibility criteria and amounts should be carefully reviewed․ The Earned Income Tax Credit (EITC) provides substantial relief to low-to-moderate income workers․ Additionally, the Child and Dependent Care Credit assists with expenses related to childcare, enabling workforce participation․ As the gig economy expands, understanding credit eligibility becomes crucial․ Given the rapid technological change and demographic shifts of 2024, staying informed about these credits is essential for maximizing tax savings and financial well-being․

Child Tax Credit Updates

The Child Tax Credit remains a cornerstone of family tax relief, but taxpayers should be aware of key changes for 2024․ While the expanded credit amounts seen in previous years have reverted, the credit still offers significant benefits for eligible families․ The maximum credit amount per qualifying child is subject to adjustments based on inflation, ensuring some level of responsiveness to economic pressures․

Income thresholds for full credit eligibility are crucial to understand, as the credit phases out at higher income levels․ Determining qualifying child criteria—age, relationship, residency—is also essential․ With the evolving economic landscape and demographic shifts of 2024, careful review of IRS guidelines is paramount․ Families navigating the gig economy or experiencing income fluctuations should pay particular attention to these updates to maximize their potential tax savings and financial stability․

Earned Income Tax Credit (EITC)

The Earned Income Tax Credit (EITC) continues to be a vital support for low-to-moderate income workers and families in 2024․ This refundable tax credit can significantly reduce tax liability and even provide a refund, offering crucial financial assistance․ Eligibility requirements are complex, factoring in earned income, adjusted gross income (AGI), and family size․

For 2024, the maximum credit amount and income thresholds have been adjusted for inflation․ Special rules apply to those without qualifying children, and age requirements must be met․ As the gig economy expands, understanding EITC eligibility for independent contractors is increasingly important․ Given the economic uncertainty of 2024, and potential for geoeconomic fragmentation, maximizing available credits like the EITC is crucial for financial well-being․ Taxpayers should utilize IRS resources and consider professional assistance to ensure accurate claiming of this valuable credit․

Child and Dependent Care Credit

The Child and Dependent Care Credit helps taxpayers offset expenses paid for the care of qualifying individuals – children under 13 or dependents incapable of self-care – to allow parents to work or look for work in 2024․ This credit is particularly relevant given demographic shifts and the increasing need for working families to balance employment with caregiving responsibilities․

For 2024, eligible expenses include those paid to daycare centers, after-school programs, or individual caregivers․ The amount of expenses that qualify for the credit is capped, and the percentage of expenses reimbursed varies based on adjusted gross income (AGI)․ As economic uncertainty persists, this credit provides vital financial relief; Taxpayers must report the care provider’s Taxpayer Identification Number (TIN) on their return․ Utilizing this credit effectively requires careful record-keeping and understanding of IRS guidelines, especially amidst broader economic changes․

Tax Implications of the Gig Economy (2024)

The expanding gig economy, fueled by digital platforms, presents unique tax challenges for independent contractors in 2024․ Unlike traditional employment, gig workers are generally classified as self-employed, meaning they’re responsible for both income tax and self-employment tax – covering Social Security and Medicare․

This necessitates careful tracking of income and expenses, as deductions for business-related costs can significantly reduce tax liability․ Key considerations include accurately reporting income on Form 1099-NEC and making estimated tax payments quarterly to avoid underpayment penalties․ The growth of the gig economy demands awareness of these obligations, particularly as geoeconomic fragmentation impacts income streams․ Understanding these implications is crucial for gig workers navigating the evolving economic landscape and ensuring compliance with IRS regulations, especially with emerging technologies facilitating these platforms․

Self-Employment Tax in 2024

Self-employment tax, encompassing Social Security and Medicare, is a significant consideration for independent contractors, freelancers, and business owners in 2024․ Unlike employees, self-employed individuals pay both the employer and employee portions of these taxes, totaling 15․3% on the first $168,600 of net earnings (for 2024)․

However, taxpayers can deduct one-half of their self-employment tax from their gross income, reducing their overall adjusted gross income (AGI)․ Accurate record-keeping of income and expenses is vital to calculate net profit subject to this tax․ With economic uncertainty and geoeconomic fragmentation impacting income, careful planning is essential; Understanding these rules, alongside the implications of emerging technologies in the gig economy, is crucial for compliant tax filing and maximizing potential deductions in 2024․

Capital Gains Tax Rates ─ 2024

Capital gains taxes in 2024 apply to profits from the sale of assets like stocks, bonds, and real estate, with rates varying based on the holding period and taxpayer’s income․ Short-term capital gains, from assets held for one year or less, are taxed as ordinary income, aligning with 2024’s tax brackets․

Long-term capital gains—assets held over a year—generally face lower rates: 0%, 15%, or 20%, depending on taxable income․ Higher earners may also encounter an additional 3․8% Net Investment Income Tax․ Considering the current geoeconomic fragmentation and economic uncertainty, investment strategies impacting capital gains require careful review․ Understanding these rates, alongside potential impacts from emerging technologies and broader economic shifts, is vital for tax planning throughout 2024․

Retirement Savings Contributions & Taxes

Retirement savings offer significant tax advantages in 2024, but the specifics depend on the account type․ Traditional IRA contributions may be tax-deductible, reducing your current taxable income, while growth within the account is tax-deferred․ However, distributions in retirement are taxed as ordinary income․

Roth IRAs, conversely, don’t offer upfront deductions, but qualified distributions in retirement are tax-free․ Given the potential for economic uncertainty and demographic shifts in 2024, maximizing retirement contributions is a prudent strategy․ Considering the impact of inflation and the evolving financial landscape, carefully evaluating contribution limits and tax implications is crucial for long-term financial security․ These considerations align with broader trends in healthcare system transformation and the green transition․

Traditional IRA Contributions

For 2024, contributions to a Traditional IRA may be tax-deductible, potentially lowering your current taxable income․ The deductibility depends on your modified adjusted gross income (MAGI) and whether you’re covered by a retirement plan at work․ Even if you can’t deduct the full amount, contributions still grow tax-deferred, meaning you won’t pay taxes on the earnings until retirement․

Understanding these rules is vital amidst economic uncertainty and geoeconomic fragmentation․ Maximizing contributions, especially considering potential inflation adjustments for 2025, can significantly benefit long-term financial planning․ This strategy aligns with navigating broader risks like misinformation and the need for strategic intelligence in a rapidly changing world․ Careful consideration of contribution limits is essential, given the evolving financial landscape and potential impacts of emerging technologies․

Roth IRA Considerations

Unlike Traditional IRAs, Roth IRA contributions aren’t tax-deductible upfront․ However, qualified distributions in retirement are entirely tax-free․ This can be particularly advantageous if you anticipate being in a higher tax bracket during retirement, aligning with concerns about future economic uncertainty and potential tax adjustments․

Considering the impact of inflation and geoeconomic fragmentation, the tax-free growth of a Roth IRA offers a hedge against future tax increases․ Contribution limits apply, and income limitations exist – higher earners may not be eligible to contribute directly․ As technological change accelerates and demographic shifts occur, a Roth IRA provides a stable, tax-advantaged savings vehicle․ It’s a strategic element in navigating the complexities of the 2024 financial landscape and beyond, especially given the rise of the gig economy․

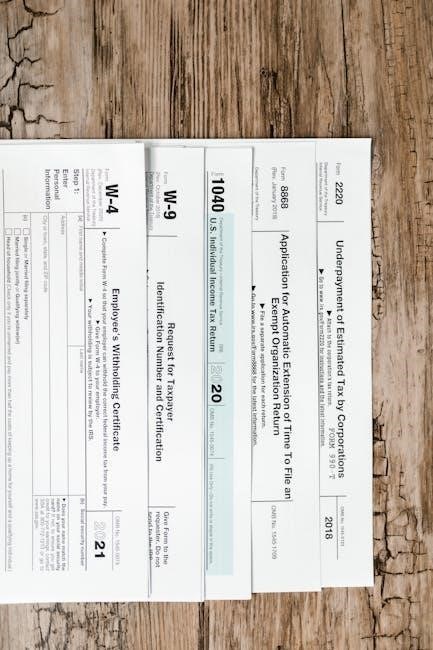

Understanding Tax Form W-2 (2024)

Form W-2, “Wage and Tax Statement,” is a crucial document for most employees․ Received from your employer by January 31st, 2025, it details your annual wages and the amount of taxes withheld from your paycheck – including federal income tax, Social Security, and Medicare taxes․ Accurate W-2 information is essential for filing your 2024 tax return correctly, especially considering the evolving economic landscape and potential adjustments due to inflation․

Carefully review your W-2 for any discrepancies, such as incorrect Social Security numbers or wage amounts․ These errors can delay your refund or trigger an IRS notice․ With the increasing prevalence of the gig economy and emerging technologies impacting employment, understanding your W-2 remains fundamental, even if you also have income reported on a 1099-NEC․ It’s a cornerstone of responsible tax filing in 2024․

Tax Form 1099-NEC: Independent Contractor Income

Form 1099-NEC, “Nonemployee Compensation,” reports payments made to independent contractors, freelancers, and self-employed individuals․ If you earned $600 or more from a single payer in 2024, you’ll likely receive this form by January 31st, 2025․ Unlike employees receiving a W-2, independent contractors are responsible for paying self-employment tax – covering both the employer and employee portions of Social Security and Medicare․

The growth of the gig economy means more taxpayers are navigating 1099-NEC income․ Remember to accurately report this income on Schedule C (Profit or Loss from Business) of Form 1040․ Deducting business expenses is crucial to reduce your tax liability․ Keep meticulous records, as emerging technologies and digital platforms increasingly facilitate these transactions, demanding careful tracking for accurate 2024 tax filing․

Estimated Tax Payments for 2024

If you anticipate owing $1,000 or more in taxes for 2024 – beyond withholdings from a W-2 or pension – you’re generally required to make estimated tax payments․ This applies particularly to those with income from self-employment, investments, or other sources not subject to regular withholding․ Payments are typically made quarterly, with deadlines in April, June, September, and January of the following year․

The increasing prevalence of the gig economy and diverse income streams necessitates careful planning for estimated taxes․ Underpayment penalties can apply if you don’t pay enough tax throughout the year․ Considering the economic uncertainty of 2024, accurately estimating income and adjusting payments accordingly is vital․ Utilize IRS Form 1040-ES to calculate and submit your estimated tax payments, ensuring compliance and avoiding potential fines․

Tax Filing Deadlines for 2024

For most taxpayers, the deadline to file your 2024 federal income tax return is April 15, 2025․ However, this date can shift slightly if it falls on a weekend or holiday․ It’s crucial to be aware of these dates to avoid penalties and interest charges․ Those requesting an extension will generally have until October 15, 2025, to file, but this does not extend the time to pay any taxes owed – payment is still due by the original April deadline․

Given the complexities of the 2024 tax year, influenced by economic shifts and emerging technologies, staying organized and filing on time is paramount․ Remember that state filing deadlines may differ from the federal schedule․ Proactive planning and utilizing available resources, like tax software or a professional, can streamline the process and ensure timely compliance with all applicable regulations․

Impact of Inflation on 2024 Taxes

Inflation significantly impacted the 2024 tax year, primarily through adjustments to tax brackets and standard deduction amounts․ As inflation cooled down, taxpayers can anticipate relatively minor changes in these areas for 2025, but the effects of 2024’s higher prices are still relevant․ These adjustments are designed to prevent “bracket creep,” where inflation pushes individuals into higher tax brackets even without a real increase in income․

Furthermore, inflation influences itemized deductions, potentially increasing the value of certain deductions․ Understanding these adjustments is crucial for accurate tax preparation․ The economic uncertainty of 2024, coupled with geoeconomic fragmentation, necessitates careful consideration of how inflation has affected your financial situation and, consequently, your tax liability․ Staying informed about these changes is key to maximizing potential tax savings․

Emerging Technologies & Tax Implications (2024)

The rapid advancement of emerging technologies, particularly Artificial Intelligence (AI), presents novel tax challenges in 2024․ AI’s impact on digital jobs and the gig economy necessitates a re-evaluation of income reporting and tax compliance for freelancers utilizing digital platforms․ The increasing use of these platforms for short-term services and asset-sharing requires careful attention to 1099-NEC reporting․

Furthermore, the development of new technologies raises questions about the taxation of digital assets and the potential for increased tax fraud through sophisticated methods․ The World Economic Forum highlights technological change as a major driver impacting the global landscape, demanding proactive adaptation from both taxpayers and the IRS․ Understanding these implications is crucial for navigating the evolving tax environment in 2024 and beyond․

Resources for Taxpayers (IRS Website & More)

Taxpayers have access to a wealth of resources to assist with filing their 2024 returns and understanding complex tax laws․ The Internal Revenue Service (IRS) website (irs․gov) remains the primary source for forms, instructions, and official guidance․ It offers tools like the Taxpayer Digital Communication, enabling secure online interactions․

Beyond the IRS, numerous reputable organizations provide tax assistance․ Taxpayer Assistance Centers offer in-person support, while Volunteer Income Tax Assistance (VITA) and Tax Counseling for the Elderly (TCE) provide free tax help to those who qualify․ Additionally, professional tax preparers, CPAs, and enrolled agents can offer personalized advice․ Staying informed about emerging risks, like misinformation, is vital, and utilizing credible sources ensures accurate filing and compliance in 2024․

Common Tax Mistakes to Avoid in 2024

Successfully navigating the 2024 tax season requires diligence and attention to detail to avoid costly errors․ A frequent mistake is neglecting to report all income, including earnings from the growing gig economy and digital platforms․ Incorrectly claiming deductions or credits, particularly those related to the Earned Income Tax Credit or child tax benefits, is another common issue․

Failing to keep accurate records, such as receipts for itemized deductions, can lead to disallowed claims․ Miscalculating capital gains taxes or overlooking changes in tax laws due to economic shifts and inflation adjustments also pose risks․ Given the rise of misinformation, verifying information from credible sources like the IRS is crucial․ Proactive planning and careful review can minimize errors and ensure compliance in this year of uncertainty․